Pension Costs Must be Proactively Managed

- Dec 30, 2021

- 3 min read

Pension Costs are Extremely Expensive

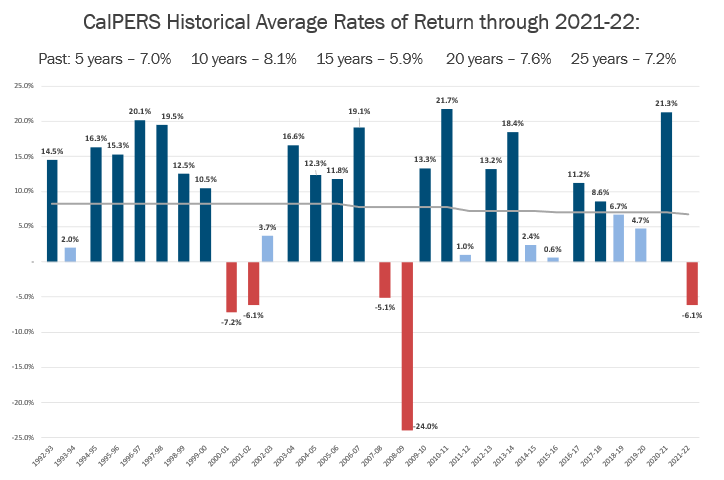

Pension costs are ever increasing. The current CalPERS discount rate is 6.8%, which was lowered from 7% in the last quarter of 2021. The discount rate is rate charged to agencies for the cost of carrying unfunded accrued actuarial liability ("UAL"). Historically, CalPERS has had several years where it has not met its targeted investment returns (see chart below). Each time this happens new UAL is created which gets paid back by agencies over 20-years at the current rate of 6.8%, all of which must be paid by the agency and not from employees.

UAL is debt, but it also represents the benefits already earned by current and former employees but not yet paid by the agency. CalPERS makes assumption changes at the beginning of each year and adjusts each agency's pension costs accordingly. While UAL is largely created by poor investment returns, there are several other assumptions (such as to retirement age, mortality rates, projected salary increases attributed to inflation, raises, increases in retirement benefits, cost-of-living adjustments, valuation of current assets, etc.) that if missed also create UAL.

In an effort to assist agencies in managing the volatility of swings in market valuation, CalPERS uses a "ramping" structure to smooth newly created UAL debt over a 5 year or longer period. While the ramping structure helps agencies with budget predictability, it also delays repayment which adds significant additional interest costs.

Pension Management Policy is Key

Weist Law emphasizes the importance of developing a robust Pension Management Policy ("Pension Policy") as the first steps towards managing your pension costs. A Pension Policy is the key building block to achieving and maintaining a healthy funding status. Most actuaries define a healthy funded ratio/status as being at least 90%. However, the difference between 90% and 100% is still very expensive debt (6.8% rate), and therefore agencies should leverage a range of tools to proactively manage these liabilities, including all potential mitigation strategies as well as an IRS-designated 115 Trust in addition to adopting a strict Pension Policy. A Pension Policy helps create a comprehensive management framework that serves as a roadmap for current and future staff, boards, and councils to make incremental changes that will lead to exponential savings and budget predictability when proactively managed annually.

Cost Mitigation Measures

Weist Law has worked with hundreds of agencies resulting in the development of over twelve different cost mitigation strategies, along with the integration of a 115 Trust, all designed to reduce long-term pension costs and achieve and maintain a healthy funded status. Each cost mitigation measure should be incorporated in a Pension Policy so that each year such opportunities do not get overlooked. Once a Pension Policy has been established, disciplined ongoing proactive management is the only viable solution. Unfunded liability evolves over time. There is no one-time fix or solution. We believe that the creation and adoption of a customized pension management plan/policy is the first step down the long path of achieving and maintaining healthy pension plans.

OPEB Should also be Proactively Managed Pursuant to Policy

Other post employment benefits ("OPEB") refers to those benefits other than pension benefits such as health care benefits, life insurance, long term care and other benefits. In June 2004, the Governmental Accounting Standards Board issued GASB 45, "Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions," that established an interest in funding options for OPEB.

Under GASB 45, an annual required contribution is determined for each municipality. The annual required contribution is a sum of the normal costs for the year (the present value of future benefits being earned by current employees) plus amortization of the UAL, using an amortization period of not more than 30 years. If an agency contributes an amount less than the annual required contribution, a net OPEB obligation will result.

Agencies have a number of options to consider in addressing their OPEB liability including: developing an internal specialized reserve fund to be considered as pay-as-you-go for GASB 45 purposes and utilizing OPEB bonds or 115 trusts, all of which should be proactively managed pursuant to a Pension Policy.

How We Can Help

Weist Law has years of experience developing innovative pension policies and cost mitigation strategies that can be used to effectively manage pension UAL and OPEB costs.

If you are interested in learning more about our cost mitigation strategies and pension policy development work and how we could assist your agency, please feel free to schedule a free consultation with our team by clicking here.

The foregoing has been prepared for the general information of clients and friends of the firm. It is not meant to provide legal advice with respect to any specific matter and should not be acted upon without professional counsel. If you have any questions or require any further information regarding these or other related matters, please contact a designated Weist Law representative. This material may be considered advertising under certain rules of professional conduct.

Comments