CalPERS Investment Returns Deal Another Blow to Government Agencies

- Aug 2, 2022

- 4 min read

Updated: Feb 14, 2023

With Another Historically Poor Investment Year for CalPERS what can Agencies do Now

California Public Employees' Retirement System ("CalPERS"), the largest US pension fund, just reported an investment loss of negative 7.4%. This negative investment performance, coming on the heals of a strong prior year performance, represents a significant additional financial burden to public agencies. The loss leaves the overall estimated funded status of CalPERS at 72%, with a year-end value of $440 billion.

To meet long-term funding targets, CalPERS must achieve long-term returns of at least 6.8% in order to avoid creating shortfalls in the plans known as unfunded actuarial liabilities (“UAL”). With last year’s sizeable investment shortfall, the loss amounts to a total miss of 14.2% for all plans. In these situations, California's state and local governments participating in CalPERS will be required to make up for the loss with funds that might have otherwise been spent on essential services, local projects, and other budgetary items.

This new UAL is a debt to these public agencies and is amortized over 20 years at the discount rate of 6.8%—far and away the most expensive debt of any government agency. This latest investment miss will result in new UAL showing up on CalPERS Valuation Reports in July of 2023. Unfortunately, the positive results that agencies will see when they open their July 2022 Valuation Reports (because of last year’s positive 21.3% returns) will be completely eliminated in the 2023 reports due to this year’s historically poor investment year. On top of that and to make matters worse, significantly more UAL will be created, leading to further declines in funded levels for all agencies.

Unprecedented Global Financial Markets

Last year’s historically bad investment year can be blamed mostly on the current state of global financial markets, including geopolitical instability, the inflationary environment, and domestic interest rate hikes which have created unprecedented market headwinds. CalPERS Chief Investment Officer Nicole Musicco stated, "This is a unique moment in the financial markets, and we've seen a deviation from some investing fundamentals."

Volatility in equities and fixed income markets led to the $12.9 billion loss for CalPERS. More specifically the drop was driven by a 13.1% decline in publicly traded stocks and a 14.5% decline in fixed-income securities. On the other hand, private equity assets resulted in a 21.3% positive return, and real assets returned a 24.1% return.

* Private market asset valuations lag one quarter and are as of March 31, 2022.

The last major CalPERS negative return was in 2009 during the financial crisis when the entire portfolio saw a 23.4% loss. During the Great Recession, the loss took CalPERS from a funded level of 101% to just 61%. Since then, CalPERS has been striving to improve their earnings to a healthy funded ratio but have only managed to gain 11% over the past 14 years, even though agencies are being asked to contribute increasing amounts towards their plans.

History Provides Clues to Possible Future Performance

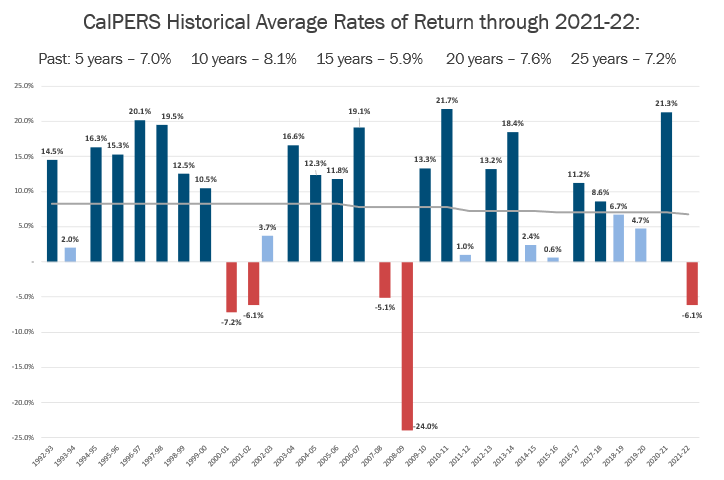

Analyzing pension investments requires a long-term view. Over the past 15 years, CalPERS has achieved annualized average investment returns of approximately 5.9%, with the 20-year average being approximately 7.6% (see chart below). Unfortunately, there is no way to predict future investment returns, but by using history as a guide, one might reasonably expect future average returns of between 5.9% and 7.6%. On the low end (5.9%), UAL would continue to grow over time resulting in increasing financial burdens on public agencies. On the high end (7.6%), UAL would decline slightly over time, but would continue to be an expensive burden to agencies as they incur the 6.8% interest cost on the UAL while the liabilities remain outstanding.

For agencies that have defined benefit programs with CalPERS, unfunded liability, or UAL, is very expensive. Pension plans should be 100% funded—agencies have a legal obligation to provide 100% of the pension benefits promised to retirees/pensioners. To the extent plans are not 100% funded, agencies must carry the financial burden (i.e., 20-year debt at 6.8%).

What Steps Can Agencies Take to Mitigate Situation

Weist Law, with decades of experience working on complex pension matters, emphasizes the importance of developing and adopting a robust Pension Liability Management Policy ("Pension Policy") as a first key step toward managing pension costs. We believe a detailed Pension Policy provides management with an effective management tool and is the key building block to achieving and maintaining a healthy pension plan funded ratio/status.

Most actuaries define a healthy funded ratio/status as being at least 90%. However, the difference between 90% and 100% is still very expensive debt (6.8% rate), and therefore agencies should leverage a range of tools to proactively manage these liabilities, including all potential mitigation strategies as well as an IRS-designated 115 Trust in addition to adopting a strict Pension Policy. Pension Policies should serve as a roadmap for current and future staff, boards, and councils to make incremental changes that will lead to exponential savings and budget predictability when proactively managed annually.

Weist Law has worked with hundreds of agencies resulting in the development of over twelve different cost mitigation strategies, along with the integration of a 115 Trust, all designed to reduce long-term pension costs and achieve and maintain a healthy funded status. Each cost mitigation measure should be incorporated in a Pension Policy so that each year such opportunities do not get overlooked. Once a Pension Policy has been established, disciplined ongoing proactive management is the only viable solution. Unfunded liability evolves over time. There is no one-time fix or solution. We believe that the creation and adoption of a customized pension management plan/policy is the first step down the long path of achieving and maintaining healthy pension plans.

If you are interested in learning more about our Pension Policy and cost mitigation strategies, please click here to sign up for a free consultation.

The foregoing has been prepared for the general information of clients and friends of the firm. It is not meant to provide legal advice with respect to any specific matter and should not be acted upon without professional counsel. If you have any questions or require any further information regarding these or other related matters, please contact a designated Weist Law representative. This material may be considered advertising under certain rules of professional conduct.

Comments